Google Cuts The Line

Google front-runs the AI IPO wave with a vertically integrated, Berkshire-blessed version of the AI trade

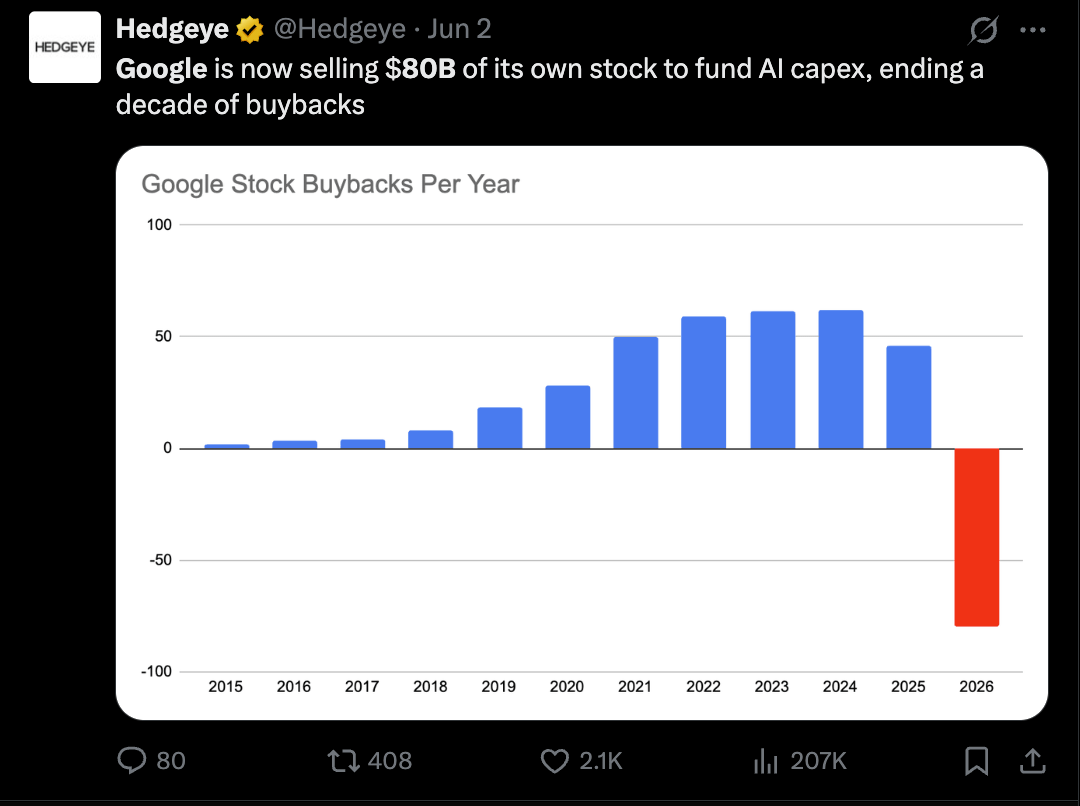

As SpaceX, Anthropic, and OpenAI wait in the wings, Google has walked onstage and announced an $80 billion equity raise, the largest stock sale in history.

For context, the largest IPO to date was Saudi Aramco in 2019, which raised roughly $29 billion. SpaceX is reportedly planning to raise $75 billion. OpenAI and Anthropic raised $122 billion and $65 billion, respectively, in their most recent private rounds, which means the private AI market is already treating “largest IPO ever” as a rounding error.

Neither OpenAI nor Anthropic has disclosed how much they plan to raise when they go public, but assume something in the $75 billion to $100 billion range and you quickly get to a strange place: roughly $350 billion-plus of capital demand from just four AI-adjacent offerings. Add the IPOs that have already happened this year, and the market may be staring at $400 billion-plus of new equity supply. Less window reopening, more dam breaking.

It is also a remarkable reversal for a market that spent the last two years begging for liquid ways to play the AI trade. We are about to go from hunger to indigestion.

To put the flood in context, the IPO market raised about $44 billion last year. The best IPO year on record was 2021, when companies raised around $140 billion. The market is now being asked to absorb ~3x the best year ever and ~10x last year’s issuance, largely around one theme.

Which raises the obvious question: where does the money come from? Investors are not usually sitting on $400 billion of idle cash labeled “AI destiny.” To buy something, they often have to sell something. So what gets sold? Do investors trim the current winners of the AI trade, like Nvidia, Broadcom, semis, cloud, and high-multiple software, to buy the next generation of AI names? Do they rotate out of defensives and go all-in on the capital-intensive AI complex? Or do these offerings simply not clear at the valuations their bankers have been whispering into pitch decks?

However that uncertainty plays out, Google has done the smart thing: it cut the line before investor exhaustion sets in. Google is pulling capital out of the ecosystem before Anthropic, OpenAI, SpaceX, and everyone else can get to it. In a world where the pool of AI-hungry capital is finite, being first is an invaluable scheduling advantage.

This is not because Alphabet cannot afford its AI ambitions. Alphabet is one of the most cash-generative companies in history. It generated $174 billion of operating cash flow over the last twelve months. This is not a company passing a hat around Sand Hill Road.

But why use debt or balance sheet cash when public markets seem so willing to throw cheap capital at the AI trade? It’s not a bad idea to capitalize on the insatiable market demand for AI exposure. Give the people what they want.

Google’s move is clever because it steps in front of the pure-play AI names and says, in effect: you want AI upside? Fine. Buy ours.

The pure-play AI names may have more narrative torque, but Google has more ways to survive being wrong. If AI margins disappoint, Google still has Search. If enterprise AI adoption takes longer, Google still has YouTube. If model prices collapse, Google still has distribution. If capex gets ugly, Google still has cash flow. Google is trying to turn the conglomerate discount into downside protection.

It is also trying to change the comp set. By raising now, Alphabet effectively forces investors to compare it with the coming AI IPO class. If the market is willing to underwrite SpaceX, Anthropic, and OpenAI as once-in-a-generation platforms, Google can ask a reasonable and slightly rude question: what exactly do you think we are?

As part of the raise, Alphabet is selling $10 billion of stock to Berkshire in a private placement. This takes an aggressive AI infra financing and wraps it in the comforting aesthetic of Omaha. Yes, this is an arms race for artificial intelligence, but Warren Buffett’s firm is nearby, so perhaps it is actually value investing.

An anchor investor matters for credibility. In a market about to be stuffed with giant AI offerings, the presence of Berkshire says: this deal has adult supervision.

The AI boom is entering its capital markets phase. That is usually when things get more interesting, more expensive, and more dangerous.

The first phase was model envy. The second phase was product panic. The third phase is balance sheet warfare. Google just fired first.

I'll tell you where the money is coming from: clueless 401ks, pensions, and retirees invested in ETFs who will be forced to buy a dog with fleas like SpaceX. Plus, private capital already has huge exposure to the upcoming CapEx nightmare.

Excellent analysis! The first mover advantage is both brilliant and evil from financially strong Google!

Liquidity does not appear out of thin air. Anthropic & Co may face a few hurdles when it’s their turn to raise capital.